Taking too long? Close loading screen.

Compare over 20 mortgage insurance policies in as little as 5 minutes.

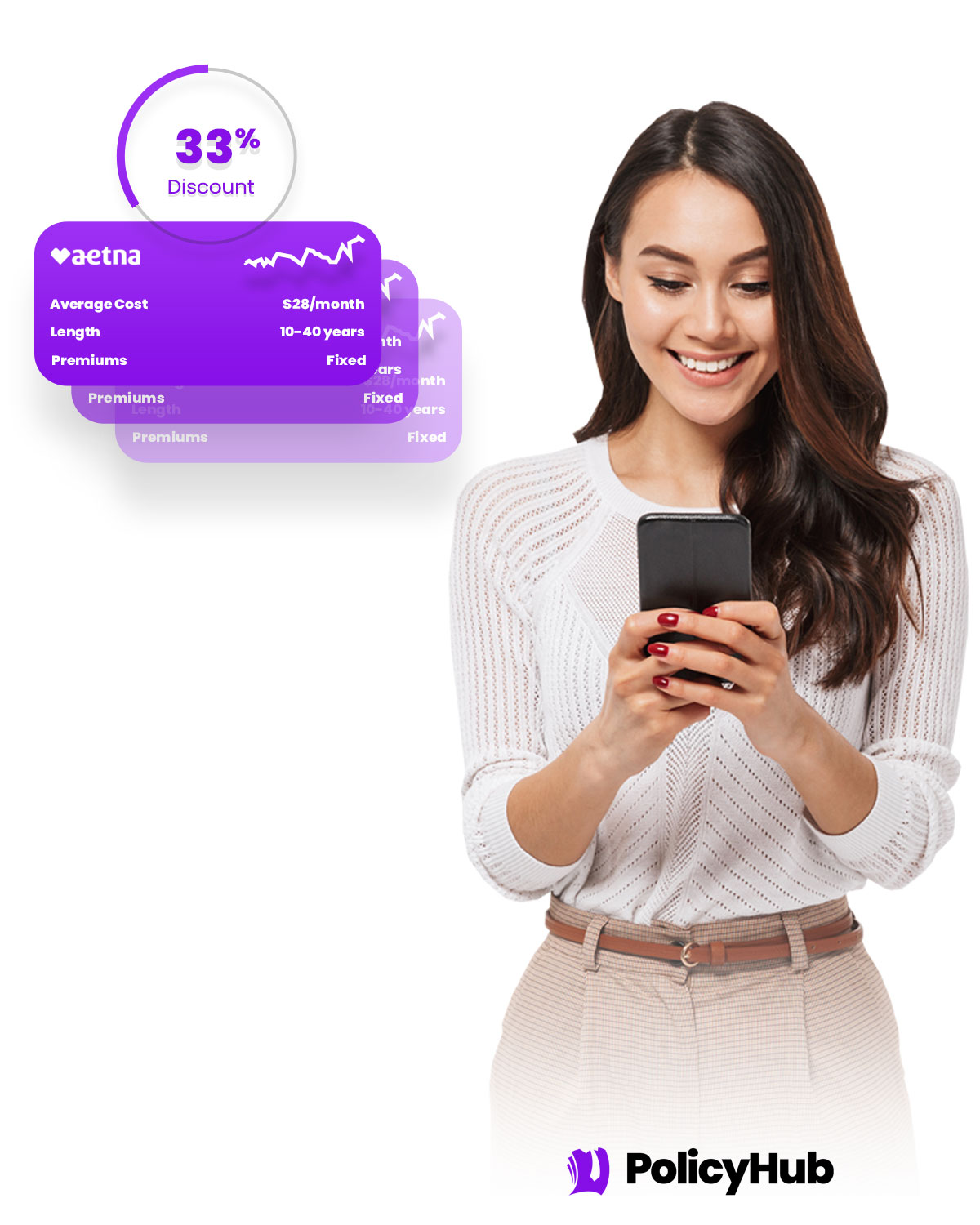

With PolicyHub you get to compare over 20 mortgage insurance policy providers in as little as 5 minutes. Save time. Save big. Get started now.

Compare over 20 top providers in Hampton Bays, NY

Your one-stop-shop to compare all the rates, all at once.

With PolicyHub you get:

Over 20 policy provider comparison.

Explore multiple Hampton Bays, NY policies from all the leading insurers and choose the one that fits your needs.

Locked in rate discount and exclusive deals.

Benefit from exclusive deals offered only to residents of your state, and lock in huge rate discounts.

Customized policies just for you.

Our team tailors policies to your unique needs, meaning optimal coverage at competitive rates.

"I was totally lost trying to find the right mortgage insurance until I found PolicyHub. I was able to work with a licensed agent to compare all my options all at one. I got the perfect plan for me at a cheaper rate than I expected."

Barbara Winters

Policy Holder

ATTN: 2024 rates just released!

Get the latest mortgage insurance rates for 2024 and lock in your policy today! Get started comparing policies today.

Get the perfect plan with the cheapest rates in 3 easy steps.

Done in 3 easy steps

Step 1

Tell us about yourself.

Finding the perfect mortgage insurance policy starts with answering a few questions to help us serve you better.

Step 2

Compare rates & plans with a pro.

Discuss your options with a licensed insurance agent. Compare different plans to find the best policy with the cheapest rates.

Step 3

Lock in cheap rates.

Secure the lowest rates and lock in the perfect mortgage insurance policy for you and your family.

"I lost hope trying to find a mortgage insurance policy that wasn't insanely expensive. Thankfully PolicyHub helped me find the perfect policy that is affordable with high coverage. Thank you!"

Bill Barton

Policy Holder

PolicyHub is the smartest way to protect the people that matter most.

Safeguard Your Family

Mortgage insurance means safeguarding your family in a worst-case scenario. Don't risk it.

Gain Peace of Mind

Far too many Americans are financially blindsided by the death of a loved one. But not your family.

Protect Your Business

Protect your business by ensuring a smooth transition of ownership with the right mortgage insurance.

Beat Estate Taxes

Inheritance or estate taxes is burdensome for your heirs. A mortgage insurance policy can help.

Invest in Your Future

For less than $1 per day, you can make a huge contribution to your family's financial safety.

Build Your Legacy

Through a mortgage insurance policy, you can leave behind a legacy for your loved ones.

Get started in less than 5 minutes.

With PolicyHub getting started is easy. Compare all the rates from all the providers. Get started in under 5 minutes.

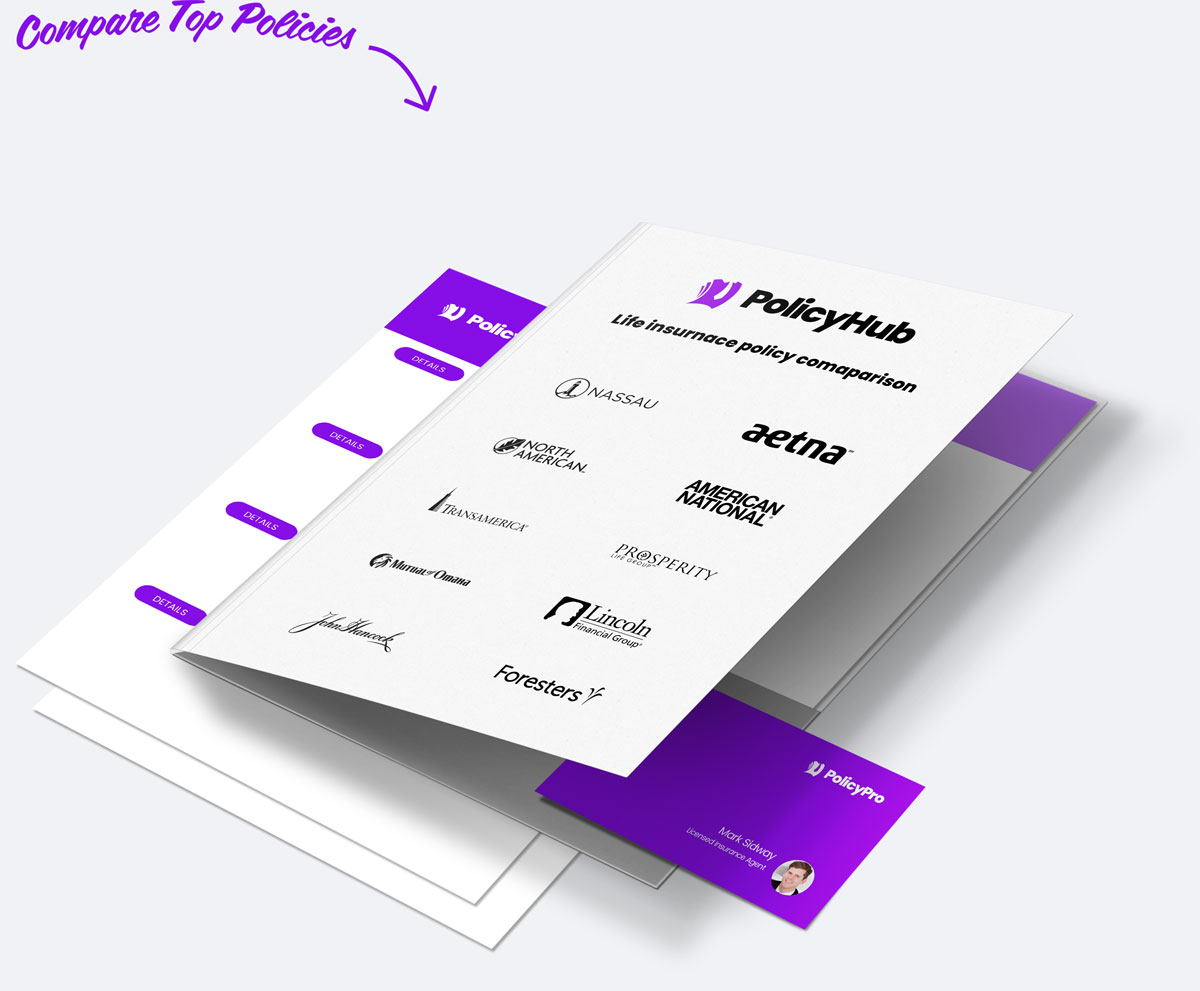

All your mortgage insurance needs in one place.

Private Mortgage Insurance (PMI)

PMI is your solution for buying a home with less than 20% down. It protects your lender, but also enables you to own a home sooner with less upfront cash. It's added seamlessly to your monthly mortgage payments.

FHA Mortgage Insurance Premium (MIP)

FHA's MIP is ideal for those with less-than-perfect credit scores. With an upfront premium and a smaller annual premium, MIP makes homeownership more attainable for a broad range of buyers.

USDA Mortgage Insurance

USDA Mortgage Insurance is tailored for rural homebuyers. With a manageable upfront guarantee fee and a low annual fee, it's a cost-effective way to secure your countryside dream home.

VA Funding Fee

The VA Funding Fee, unique to VA home loans, is a one-time fee that helps sustain the VA loan program for future generations of military homeowners. Depending on your service history, you may even be exempt.

"Highly HIGHLY recommend PolicyHub if you need mortage insurance. They saved me sooo much time and money on my policy, it's nuts. Comparing all the providers at once is a game changer."

Chris Stephens

Policy Holder

Introducing PolicyHub Price Match Guarantee

Our priority is to save you money while getting you the right coverage. If you find a lower rate for a similar policy anywhere else, we'll match it! With PolicyHub, you can rest assured knowing you're getting the best price.

Save time and get the best policy with the cheapest rates. Guaranteed.

| Option 1 | Option 2 | |||

|---|---|---|---|---|

| 100% Digital | ||||

| Licensed Agents | ||||

| Expert Support | ||||

| Get Started in 5 Minutes | ||||

| Decades of Experience | ||||

| Compare 20+ Providers | ||||

| Zero Hidden Costs | ||||

| Top Insurance Providers |

"I knew I needed mortgage insurance but I didn't know where to go. I talked with a few other companies but the cost was outrageous. I found PolicyHub and found the perfect plan for me at an affordable cost."

Wendy Smith

Policy Holder

Frequent Questions...

Mortgage insurance in Hampton Bays, NY is an important part of homeownership and helps protect lenders in the event that the borrower defaults on the loan. It generally comes in two forms: private mortgage insurance (PMI) or mortgage insurance premium (MIP). PMI is generally required if the down payment on the home is less than 20%, while MIP is typically required for FHA loans. Premiums are based on factors such as the size of the loan and the size of the down payment.

What is the minimum down payment to avoid a Hampton Bays mortgage insurance policy?

In the Hampton Bays, NY area, the minimum down payment to avoid mortgage insurance is typically 20%, although homebuyers may find certain scenarios in which an even higher down payment is required. That said, the average down payment for new homebuyers is anywhere between 3 and 20%, so it is important to check with lenders in the Hampton Bays area to determine what is right for you. Most lenders will offer various options to avoid mortgage insurance, but in most cases, paying 20% or more as a down payment is required.

Do I need a private mortgage insurance policy Hampton Bays?

While it is not mandatory in every circumstance, private mortgage insurance (PMI) may be required if you do not put a 20% down payment on the property you are purchasing in Hampton Bays, NY. PMI protects your lender in the event of default, and is usually a monthly added expense for the loan. Generally, if you do not put down 20% of the loan amount up front, a lender may require you to purchase PMI. Depending on your particular circumstances, purchasing PMI might be the right option for you and could enable you to get into a home sooner.

What are the drawbacks of FHA mortgage insurance near Hampton Bays?

While FHA mortgage insurance can be a great tool for those in Hampton Bays, NY, looking to purchase a new home, there are still drawbacks to consider. The most notable is the cost of the insurance FHA mortgage insurance often comes with a higher up-front cost than a conventional loan, and could also require monthly premiums for the duration of the loan. Additionally, FHA mortgage insurance typically requires that the borrower has good credit, as well as a source of steady income, which could limit eligibility.

How do Hampton Bays mortgage insurance companies process USDA insurance?

USDA mortgage insurance in Hampton Bays, NY protects lenders from any loss in case a borrower fails to make their payments. Borrowers only need to have a minimum credit score to qualify for this insurance and are subject to payment of a guarantee fee at the closing of the loan and annually after that. The overall USDA guarantee fee can vary depending on the size of the loan but typically ranges from 1% to 2%. This guarantee fee is fully financed in the loan that makes the borrower not responsible for paying the fee directly.

The VA funding fee in Hampton Bays, NY is based on various factors including the Veterans military category, loan amount and loan type. For Veterans that have served previously, the fee is usually a one-time flat fee of 2.3% of the loan amount. For Veterans who are currently serving or have served within the last three years, the fee is slightly higher at 3.6%. These rates may slightly fluctuate based on your military status. Additionally, Veterans who receive VA disability benefits are exempt from the VA funding fee entirely.

What factors influence the cost of mortgage insurance in Hampton Bays?

The cost of mortgage insurance is often determined by a number of factors, such as credit score, the amount of money being borrowed, the loan-to-value ratio, the type of loan, and the property location. Specifically in Hampton Bays, NY, mortgage insurance cost could be influenced by the state and local taxes in the region due to the cost of living in the area as well. In addition, the availability of mortgage insurance in the area might influence the cost, as certain companies may not offer policies in more rural markets.

What process do I need to follow to cancel my Hampton Bays mortgage insurance policy?

To cancel your mortgage insurance in Hampton Bays, NY, you should contact your lender or servicer directly. If your loan was insured by the Federal Housing Administration, you would need to provide documentation proving you have at least 20% equity in your home in order to cancel the insurance. If the insurance was purchased privately, you would need to contact the insurer to get specifics on the cancellation process. You can also contact the local Hampton Bays Town Clerk for additional resources regarding the cancellation process.

Is the mortgage insurance calculation method the same for every Hampton Bays mortgage insurance company?

In Hampton Bays, NY, the mortgage insurance calculation method will vary among lenders. Depending on the lender, you may have a slightly different experience in calculating the mortgage insurance for your loan. It's always a good idea to discuss your mortgage insurance with your lender ahead of time to make sure that you are aware of any potential differences in the calculation methods and so that you can be sure that you're fully informed when making decisions about your mortgage.

Are there alternatives to mortgage insurance companies in Hampton Bays?

Yes, there are alternatives to mortgage insurance in Hampton Bays, NY. Homeowners can look into a variety of loan products that qualify for lower than normal down payments. Some federally insured loans and local banks may even eliminate the need for mortgage insurance due to the owner occupants' higher credit scores. All of these options should be discussed with a qualified mortgage advisor prior to making a decision to ensure the best financial fit.

Compare Life Insurance Policies

Get started today and compare over 37 life insurance providers in as little as 15 minutes.

© 2024 PolicyHub - all rights reserved